The reputation and cultural challenges facing Boeing

Trust in Boeing is damaged after yet another safety issue. Repairing its reputation and regaining the trust of regulators, airlines, and passengers is going to be tough and requires a strategic rethink and refocus.

What was once a giant of the skies is today seen as an example of how to avoid running a company. Boeing needs to redesign its culture and deliver.

Here is an example of a failed management culture that focused blindly on shareholder value to the extent that design, innovation, and even safety have been compromised.

The 2019 tragedies involving the 737 Max raised serious questions about Boeing's commitment to safety, its design processes, and the initial certification of the 737 Max,

In January this year, the near tragedy of the Alaska Air flight, which lost a door-shaped panel mid-air, confirmed that for all the words and the strong PR and stakeholder engagement that was leveraged after the tragedies years back, nothing has changed.

One CEO left, and another one took over. Words were shared, but actions still need to be improved, impacting its reputation amongst multiple stakeholders.

So, let’s look at the issues and see what the airline can do to repair its crumbling reputation.

Safety Concerns

The two fatal crashes involving the 737 Max in Indonesia in 2018 and Ethiopia in 2019 led to the worldwide grounding of the aircraft.

Management worked hard to reassure airlines, regulators and passengers. But even its communications and engagement strategy, which former CEO Dennis Muilenburg deployed then, could have been better.

Boeing rolled out software updates and training enhancements for the 737 Max, hoping to help repair confidence in this aircraft. All this appeared to be paying off until the recent issue with Alaska Airlines, where the failure to install bolts to keep a door-shaped panel in place correctly highlighted more significant problems within the company.

Regulatory Scrutiny

The incidents from 2018/19 brought intense scrutiny from aviation regulators globally. The Federal Aviation Administration (FAA) in the United States and other international regulatory bodies undertook extensive reviews of the 737 Max, leading to significant delays in recertification.

The FAA, which initially certified the 737 MAX, came under fire for its oversight and relationship with Boeing. Investigations suggested that the FAA had delegated too much authority to Boeing for the certification process. This led to a re-evaluation of the certification process and increased oversight.

Meanwhile, the European Union Aviation Safety Agency (EASA) independently reviewed the 737 MAX before allowing it to return to European service. It marked a departure from generally following the FAA's lead and indicating a shift towards more autonomous regulatory action within the European Union.

Aviation regulators in countries like China, Canada, Brazil, and others also assessed the 737 MAX and Boeing's proposed fixes. This global response indicated a growing trend where national regulatory bodies assert more independence in aviation safety standards today.

Corporate Governance and Leadership Accountability

The recent crisis and comments about the culture within Boeing raised further concerns about the company’s internal governance and whether it had the management in place to make changes to deliver confidence to its various stakeholders.

Criticism was directed at Boeing's past and current leadership, including CEO Dave Calhoun, for handling the issues and the perceived initial lack of transparency. This has led to calls for improved oversight and changes in leadership approach.

With Boeing competing with Airbus, questions are being asked about the culture at the top of the company and if their priority was shareholder value and growth, leading them to cut investment in areas that impacted aircraft delivery.

Equally, in 2022, Boeing reported spending $2.6 billion on research and development. This was down from $3.4 billion spent in 2021. This is less than what the €3.49 ($3.78 billion) billion Airbus invested in the same year.

Boeing's level of investment is less than Airbus’s, partly due to the repercussions of the 737 Max tragedies and their impact on its order book. Yet, even taking that into account, Airbus is committed to elevating R&D spending in coming years to maintain its competitive edge, meet climate goals, and develop next-generation technologies in aerospace.

Financial Impact

Boeing suffered financially due to the grounding of the 737 Max, with costs running into billions of dollars due to compensation claims from airlines and suppliers, production halts, and delayed deliveries.

It’s worth pointing out that Boeing's stock is primarily owned by institutional shareholders, with major investment groups holding a significant portion of shares. As of late 2023 and early 2024, the top institutional shareholders include Vanguard Group Inc., BlackRock Inc., Newport Trust Company LLC, State Street Corp, FMR LLC, Capital World Investors, and Capital Research Global Investors. These organisations hold substantial stakes, ranging from around 1.7% to 7.87% of Boeing's shares.

In addition to these institutional investors, a smaller percentage of the stock is held by insiders within the company, and retail investors own a considerable portion. This diversified ownership structure is typical for large publicly traded companies like Boeing.

The issues from 2018/19 and now 2023/24 are affecting its order book, with many US and international airlines rethinking their orders or looking to renegotiate the existing relationship. Even United Airlines has cast doubt on the 737 Max 10 order after Boeing’s recent problems.

Customer and Stakeholder Trust

Restoring trust with airlines, passengers, and other stakeholders has been a major challenge. As Boeing's direct customers, airlines have had to manage disruptions and reassure their passengers about safety.

The reputational damage that Boeing is experiencing is not exclusive to themselves. Research from Morning Consult amongst US passengers highlights that trust amongst passengers has been hit, which, in return, impacts airlines that fly this and other Boeing aircraft. The analysis of this was featured on CNBC, highlighting the huge and bringing carriers into the mix.

Currently, 11 airlines operate the Boeing 737 Max 9s: Aeromexico, Air Tanzania, Alaska Airlines, Copa Airlines, Corendon Dutch Airlines, Flydubai, Icelandair, Lion Air, SCAT Airlines, Turkish Airlines and United Airlines.

Market Competition

The 737 Max crisis coincided with increased competition from other aircraft manufacturers, notably Airbus. This has put additional pressure on Boeing to resolve the 737 Max issues and maintain its market position.

Reputational Recovery Efforts

Under Calhoun’s leadership, Boeing has undertaken efforts to rebuild its reputation, focusing on transparency, safety improvements, and engaging with regulators, customers, and the public. This includes rigorous testing, software updates, and training enhancements for the 737 Max.

For Boeing, Dave Calhoun and his senior team, navigating these challenges requires a strategic approach that prioritises safety, transparency, and effective stakeholder communication.

The long-term impact on Boeing's reputation hinges on its ability to effectively address these issues and prevent future incidents. Above anything, the culture and the corporate focus need to be addressed.

However, the leadership needs to engage with stakeholders, not just those external to the organisation.

The firm has a lack of vision and focus. With a potential culture that focuses on delivering short-term returns to shareholders, conversations must be had with these stakeholders so that they can be aware of the transformational work needed to regain the trust of regulators, airlines and passengers. Because trust in Boeing is what helps Airlines operate.

Boeing is a great airline that, sadly, is lacking vision and focus. People need to trust the aircraft, the company, and everyone involved in the manufacturing and supply chain.

Strategic counsel can deliver trust, but after the recent issues, repairing Boeing's reputation will take time, a strategic refocus and investment.

Navigating the Complexities of Stakeholder Engagement in International Markets

Trust, reputation, and cultural understanding are critical in the globalised environment in which we live and work. Where there is a lack of trust, there is a lack of innovation and growth. A new approach is needed to support innovation and growth.

Trust, reputation, and cultural understanding are critical in the globalised environment in which we live and work. Where there is a lack of trust, there is a lack of innovation and growth, and, sadly, recent data from both the World Economic Forum 2024 Risk Report and Edelman’s own Trust 2024 Barometer confirm that the level of trust that people in politics and business is low.

Yet, for some reason, not enough is being done to raise the level of trust, which is impacting the level of opportunities. Investing, not just financially but through the process and culture, in developing trust and reputation appears to be lacking.

As companies and investors work across international markets, the complexities of engaging with diverse stakeholder groups become increasingly pronounced for them. This complexity is particularly evident in sectors like technology and investment, where rapid change and high stakes are the norms and where there is a difference in regulatory and cultural norms.

So, how can governments, businesses and investors better leverage perception and reputation to support innovation and growth?

The Importance of Stakeholder Engagement

The dual pillars of trust and reputation management are at the heart of not just successful stakeholder engagement but also innovation and growth.

Trust forms the foundation of all business relationships for every organisation, influencing decisions and shaping business outcomes internally and externally.

The fact is that CEOs agree that trust is essential, even critical, in helping deliver growth is positive. In PwC’s 2023 Trust Survey, ‘91% of business executives agree that their ability to earn and maintain trust improves the bottom line. Conversely, a lack of trust can erode brand value, hurt financial performance and limit a company’s ability to attract and retain talent.’

Yet, while there is an understanding of the importance and value of trust within the C-Suite, the work needed to develop trust still appears to be done tactically rather than strategically.

Financial metrics take control of decision-making, which is understandable. But trust and reputation influence how business is done and how the other party in the relationship feels about any transaction, even in the design of products or services, and especially in the digital and technology sectors.

In this Deloitte CFO article, the firm discusses the importance of trust and how measuring trust across different operating domains can help leaders identify their organisation’s potential sources of a trust breakdown or areas where building trust proactively can help create a competitive advantage.

Building and maintaining trust and reputation must become a strategic imperative in the volatile domains of technology and investment, where the pace of change is fast, and the environment is inherently uncertain, especially in the hyper-connected world where opinions are shared, and people can influence buyers and investors.

Understanding Cultural Nuance

One of the key challenges in international markets is identifying and engaging with stakeholders and navigating the cultural nuances that influence their expectations and behaviours. For instance, what influences trust varies depending on the international market in which you are trying to do business.

This is why communications and engagement strategies need to be adapted to take into account local culture, sensibilities, norms and customs.

This article from Harvard Law School’s Program On Negotiation presents some strategies that need to be considered when engaging and negotiating.

Do homework on your international partner’s culture

Through reading and conversations with those who know the country concerned, you can certainly learn a lot. Don’t overlook your in-market partners as sources of information about their culture. They will usually welcome your interest and help the research process.

Show respect for cultural differences

Inexperienced negotiators tend to belittle unfamiliar cultural practices. It is far better to seek to understand the value system at work and to construct a problem-solving conversation about any difficulties that unfamiliar customs pose.

Respect for cultural differences will get you a lot further than ignorance, so it’s important to do your research when entering into negotiations with unfamiliar counterparts.

Be aware of how others may perceive your culture

You are as influenced by your culture as your counterpart is by his. Try to see how your behaviour, attitudes, norms, and values appear to your foreign supplier.

When you enter into negotiations, it helps to know how they see you from a cultural standpoint. You can adjust your approach during negotiations to get a better outcome if any of these perspectives are negative.

Find ways to bridge the culture gap

It is possible that cultural differences can create a divide between you and your suppliers. Constantly search for ways to bridge that culture gap.

The first step in bridge building requires you and your suppliers to find something in common, such as a shared experience, interest, or goal.

Culture is not what separates people but what makes them unique. Respect that and show interest and areas of commonality.

Reputation Management: A Cornerstone of Engagement

In reputation management, the stakes are high. Remember, managing your reputation is not a tactical activity but a strategic operation. How you are perceived matters.

A misstep can erode years of goodwill, particularly in the digital age, where information spreads rapidly through social channels.

The investment sector provides a stark example: according to research by AON, a British-American professional services and management consultancy, ‘Reputation crises offer financial markets an opportunity to re-evaluate their estimation of future cash flow and, thus, to adjust their valuation of a given company. The market receives new information about the company and its management at times of crisis and forms a consensus view as to whether the impact on long-term future cash flows will be positive (the Winners) or negative (the Losers).’

Based on our [AON] reputation research of 340 events over the last 40 years, the average impact on shareholder value has been 7 per cent over the post-event year [2023], equivalent to a total loss of USD 830 billion over and above the market.’

For venture capitalists and investors, this highlights the imperative of maintaining a solid reputation, not just for their own venturing arm but for the companies they invest in.

Due diligence needs to also focus on perception and reputational issues.

Adopting a Strategic Approach

To navigate these issues, companies must adopt a strategic approach to reputation management and stakeholder engagement.

Understanding Stakeholder Perceptions

It’s important to regularly check stakeholder perceptions and expectations through surveys and feedback mechanisms, sharing the data and insight gained from a strategic point of view with the C-suite and the Board. Stakeholders are also not just external people but also internal.

Polling, or user research, is an important source of insight for governments and opposition parties on where and what their policies should on. This post from Gallup shares six key reasons why measuring public opinion on an ongoing basis is critical.

Communication and Transparency

Maintaining open lines of communication and being transparent about business practices, especially in areas prone to public scrutiny, like data privacy and ethical investment, is critical.

Tailored Engagement Strategies

Developing engagement strategies tailored to each market's cultural and regional specifics is essential.

Building Long-term Relationships

Focusing on long-term relationship building rather than short-term gains, especially in sectors like technology and investment.

Risk Management

Proactively managing risks that can impact reputation, including operational, financial, and ethical risks.

Navigating the complexities of stakeholder engagement in international markets requires a nuanced understanding of trust and reputation management.

By learning from the successes and failures in sectors like technology and investment, companies can develop strategies that resonate with diverse stakeholder groups. In doing so, they safeguard their reputation and lay the foundation for sustainable, long-term growth.

Perception and reputation matters and boards and their C-suite need to think about this as a strategic value-add.

Why the wrong culture can stop growth

The UK and Europe are lagging behind the US in maximising the potential of tech companies founded in their respective national markets, but why?

Culture, perception and confidence are holding us. How do we resolve this?

Peter Drucker was right, "Culture eats strategy for breakfast."

Don't get me wrong, strategy is critical, but without having an understanding of people, their likes, dislikes and fears, a business is going to struggle to realise its potential or even fail.

Earlier this week, I read a great post by Gerard Grech, where he presented some data that highlighted the challenges the UK and Europe face compared to the US when it comes to growing enterprise-sized technology companies.

The UK and Europe has over 50% of the world's top 20 science and technology clusters, yet, compared to the US, we are not maximising the opportunities that we create, yet!

While we are playing catch-up, change is happening and a new environment is being created that can help us better compete and grow companies that can scale and secure value and returns. To achieve this though the whole issue needs to be looked at strategically, wit ha key focus on establishing a culture that helps deliver growth.

Of course, before all this we need to look at the differences that exist between the UK / Europe and the US.

The Differences

Investment Climate:

UK/Europe: The UK and Europe have a strong network of investors, including venture capitalists (VCs), corporate venture capital (CVCs) from enterprise-size companies, angel investors, and government funding schemes. London is a leading global tech hub, attracting a diverse range of investors. However, the total amount of venture capital available is generally smaller compared to the US.

US: The US, particularly Silicon Valley, has a larger pool of VCs and CVCs and a long-standing tradition of investing in tech startups. The investment sums are equally often larger, and there's a greater willingness to fund early-stage companies where risk is higher.

Risk Tolerance:

UK: There's a perception of lower risk tolerance in the UK. Failure is often viewed more critically, and there can be a greater fear of failure among entrepreneurs. And not that I say perception and the impact that this has amongst peers in the investment or policy-making community. The perception of failure can impact the types of ventures that receive funding, especially from the UK and European VCs and CVCs, a reason why American venture capitalists move in to fund and secure equity in so many start-ups on this side of the Atlantic. Equally, a reason why no many start-ups look to the US for investment, especially when looking for an exit or IPO.

US: American culture traditionally celebrates risk-taking and is more forgiving of failure. This attitude can lead to a higher risk appetite among investors and entrepreneurs, fostering a more dynamic startup environment. Failure is seen as a learning exercise, and the investment model takes this into account when supporting start-ups through different funding rounds.

Business Culture:

UK: The business culture in the UK is often described as more reserved and formal. Networking and relationship-building can be more subtle, and there is a strong emphasis on established business practices and protocols. Technologies and processes that are disrupted are questioned rather than supported so that they generate new market and revenue channels. Equally, how the media report failure and risk taking is quite different to that in the US.

US: American business culture is generally more direct, with a focus on quick decision-making. There's a stronger emphasis on innovation and disruption, and networking tends to be more open and aggressive. Media focus on the positive and the learnings from failure. Worth noting that it was Samuel Beckett who said, "Try Again. Fail Again. Fail Better", an ethos adopted more in the US.

Regulatory Environment:

UK: The UK is in a state of regulatory transition. However, our strong legal frameworks and consumer protections can sometimes be more stringent than in the US.

US: The regulatory environment in the US can vary greatly from state to state, but overall, there is often a more laissez-faire approach to regulation in the tech sector. However, this can vary with changing political climates. The ability to engage and lobby can be costly, ensuring that it is either the enterprise technology companies or their investors who have access and influence. Equally, the ability to take risks, while regulated, it is not capped down.

Talent Pool:

UK: The UK has a strong talent pool, particularly in areas like fintech and AI, with a good mix of local and international talent due to our world-renowned universities. These universities also create incubators that help fund innovation that can be scaled

US: The US, particularly in tech hubs like Silicon Valley, has a massive, diverse talent pool, drawing experts from around the world. However, competition for top talent is intense.

The solutions

So, how do we fix the issues that are currently preventing us from generating growth from the tech that we develop?

There are many, far too many to go through here, but one thing that cuts across is, in my opinion, culture and the perception of risk.

Let's look at some:

Redeveloping the Investment Ecosystems:

We need to continue to encourage the development of VC, CVC and angel investor networks. Wit regards to CVCs, for example, UK companies do not as yet have as many corporate venturing arms that invest in innovation or solutions from which they can secure a return. Why is that? And what can be done to resolve this? Let's remember that start-ups don't just need cash. They also need insight, knowledge and experience and, equally, access to a network of prospective users of their products. Are corporates fearful of investment in risky ventures, even through CVCs? Is this is the case, then this needs to be challeneged and incentives need to be designed to ensure so they can be part of the innovation solution.

Encouraging a Culture of Innovation:

Promoting a culture that values innovation and risk-taking. This can be achieved through public campaigns, educational reforms, and support of entrepreneurial education. Focus on the insights gained from failures that have helped businesses succeed. Changing the narrative and cultural attitudes to failure is an objective that needs to be done across many touchpoints, including education and established attitudes in work. This is very much a medium to long-term objective.

Improving Access to Talent:

Raising awareness not just of STEM education, but also financial management to ensure that businesses have access to the necessary skilled workforce that can help them grow and scale. Additionally, focusing on creating opportunities to switch jobs and move skill sets into new areas.

Research and Development Support:

Our academic community is world-leading. The knowledge and research they invest in developing and sharing with alumni need rewards, which is why their own VC units need to incentivise them to work more collaboratively.

Providing support for research and development through subsidies, partnerships with universities, and creating innovation hubs or clusters where start-ups can collaborate with researchers and established companies.

There are specific audiences who need to understand the strategy, the journey and the outcome. But they need to be influenced and incentivised to ensure that individually they support the growth of the technology and innovation ecosystem in the UK and Europe. This is no mean task, but equally, it is not impossible.

Changes are starting to take place. Specific communities are talking openly more about what they need.

Let's move at pace and learn while we deliver.

*This blog was originally posted on my LinkedIn newsletter: Reputation Matters - Why the wrong culture can stop growth. Subscribe.

The Implications Of The EU's AI Act and The Future.

The EU has moved first with with EU AI Act. Where next for innovation and growth, and what are the impacts for companies, countries and other trading blocs?

European Commissioner for Internal Market, Thierry Breton

Last week, the European Union passed its EU Act, a piece of legislation that is designed to regulate artificial intelligence. The Act aims to establish safeguards for EU citizens while enabling growth for businesses, something that is a fine line.

The impact of this piece of legislation though, won’t just be felt within this trading bloc, because, like with GDPR, it will also shape how companies outside have to shape AI if their generative tools are to be used by EU citizens.

With this Act,what the EU has done is seized the lead in terms of regulations and started a global discussion that countries and trading blocs around the world will either agree or disagree with.

But the journey to this piece of legislation started decades ago and is based on the values that the EU was founded on.

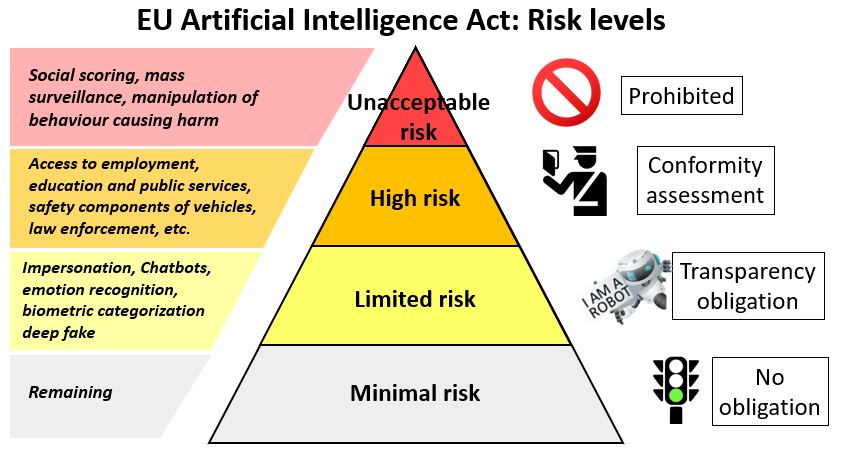

What is the EU proposing?

The EU is using a risk-based system that categorises based on identifiable risk posed. The higher the risk the stricter the regulation with a focus being on safety and the rights of the individual. For example biometric, social scoring and the like will be banned.

Transparency requirements will force those building AI models to disclose certain types of information to ensure compliance with other laws are met.

The Acts gives the EU the power for algorithmic audits and the ability to issue fines.

Where did the journey towards this deal really start?

The journey started during the early Internet days, between the 1980s and 1990s, when data was limited and primarily text-based. The focus at that time was more on connectivity and less on data accumulation.

However, during the dot-com boom of the late 90s and early 2000s, companies scaled their adoption of the Internet as a channel for commerce and communication.

During this period and over the years, search engine companies like Google and social media companies like Facebook, Twitter and YouTube grew. It was all about data capture so that advertising offers could be developed to finance growth.

In the early 2010s, the concept of cloud computing and Big Data, characterised by the 3 Vs: Volume, Velocity, and Variety, took hold. Companies began collecting and analysing vast amounts of data for insights.

The volume of data allowed the development of machine learning, particularly deep learning, which made significant advances in gaining insight from large datasets. Neural networks trained these large datasets and began to achieve impressive results in tasks like image and speech recognition.

Generative models, such as GANs (Generative Adversarial Networks), also started to emerge, capable of creating realistic images, texts, and other data forms.

Today we find ourselves at a stage where Generative AI models, like GPT (Generative Pre-trained Transformer), Bard, Claude and others, have become more sophisticated, benefiting from the accumulated vast datasets and improved algorithms.

These models have begun to find applications in various fields, from content creation to scientific research, driven by their ability to generate realistic and coherent outputs.

The pace of change in AI is incredible, leading companies and regulators to focus on the ethical implications, data privacy, and the development of more advanced, context-aware systems.

How much data are we producing today?

We are producing vast amounts of data, which is enabling the exponential growth of AI and generative AI.

On average, each person is producing approximately 1.7 megabytes (MB) of data per day or 620MB per year, a figure that by 2025 could grow to 1.5GB annually or 27 terabytes per year per person by 2025.

Today, this data comes from our internet browsing, use of mobile applications, digital purchases, social media posts, location data from smartphones, and more. However, those who are more digitally immersed and active online could be generating several times more data than the average.

Of course, in the early days of the internet, we were creating mostly text-based communication and information, which was shared among small networks of researchers and academics. AI was a mere concept.

During the 1990s, as more people started to use the internet and early search engines, we still created little data per person, maybe a few megabytes of emails, documents, and browsing history per year.

The rise of social media during the 2010s changed that as platforms encourage billions of people to share massive amounts of personal data - photos, videos, messages, interests, and behavioural data. This allowed for data generation to explode, with, on average, users creating multiple gigabytes per year.

As Big Data and AI grew, growth produces a dataset so huge that AI begins to unlock new capabilities. An average person might generate tens of gigabytes per year now with all their online activity.

Billions of people contributing leads to total global datasets in the order of exabytes and zettabytes. However, many of these datasets are siloed, so the work is being done to gather data together to help generative AI better.

But these datasets have issues around them, especially from a legal and data privacy point of view. Issues that the EU Act, as well as others that follow will look to resolve.

The issues are also around the factual content of these datasets and biases that algorithms can gather from not so much misinformation but data that is wrong and not verified. These issues can influence many specific tactical and strategic points, which impact reputation and trust.

Why are countries creating regulations for AI and generative AI?

Simple, regulation is about safety, security and business growth. But, when it comes to growth, it is also about gaining an early competitive advantage.

For example, being a leader in AI can significantly boost a country’s economic growth:

Innovation and New Industries: AI leadership fosters innovation, leading to the creation of new industries and job opportunities. It also enhances existing industries through improved efficiency and innovation

Attracting Investment: Countries and trading blocs leading in AI are magnets for investments from multinational corporations and startups focusing on cutting-edge technology

Enhancing Public Services: AI can revolutionise public services, making them more efficient and accessible, thus improving overall quality of life and economic stability

International Influence: Leadership in AI technology grants a country or trading bloc significant influence in shaping global digital policies and practices.

Singapore recently announced its own AI strategy, which is 'no longer seen as a good to have, but a must-have.' They are focusing on

Building a robust talent pool

Fostering an AI-friendly ecosystem

Encouraging public-private partnerships.

Singapore and its Singapore Economic Development Board (EDB) excel are looking strategically and across silos when it comes to strategy and designing delivery that delivers growth.

For The UK, after the recent AI Safety Summit, AI is central to it's focus on growth, with the remit held by the Department for Science, Innovation and Technology (DSIT). Yet, to secure growth, especially given the pace at which other markets are moving, what is needed is a cross-government approach.

The US, meanwhile, is going down a different route, with states taking the lead over federal regulation, even though the US President issued an Executive Order 'on safe, secure and trustworthy AI and a blueprint for an AI Bill of Rights.'

What is next for AI and generative AI?

The next phase in generative AI is expected to focus on several areas, including:

Ethical AI and Responsible Data Use: As data generation grows, so does the need for ethical considerations in AI training and usage, including privacy concerns and bias mitigation.

Context-Aware and Personalised AI: Future AI systems are expected to be more nuanced in understanding context, leading to highly personalised and accurate content generation.

Integration with Emerging Technologies: The combination of AI with other technologies like augmented reality, quantum computing, and the Internet of Things (IoT) will likely open new frontiers in data generation and utilisation.

Sustainable AI: With the increasing awareness of the environmental impact of data centres and computing resources, there will be a push towards more energy-efficient and sustainable AI practices. Chip makers like Arm are designing their chipsets with a focus on decarbonizing compute.

What risks exist in this AI race?

Countries efforts to lead in AI and generative AI, which can deliver business growth, could be undermined by:

Insufficient Investment in Research and Development: AI and generative AI are rapidly evolving fields requiring substantial investment in research and development. Failure to allocate enough resources could hinder a country's ability to stay at the forefront of AI advancements.

Talent Shortage: A lack of skilled professionals in AI and related fields can be a significant barrier. This includes not only AI researchers and developers but also a workforce capable of understanding and working with AI technologies. This issue can only be resolved through investment in education, which many countries have been leading for years.

Inadequate Infrastructure: AI technologies, particularly data-intensive ones like generative AI, require robust and modern digital infrastructures, including high-speed internet and powerful computing resources. Inadequate infrastructure can limit the development and deployment of AI solutions. Countries like the Saudi Arabia and the UAE have been doing deals to, for example, but Nvidia chips to power their AI ambitions. AI companies based in the UAE are themselved making the call on what side they will be.

Data Privacy and Security Concerns: As AI systems rely heavily on data, concerns about privacy and data security can impede their adoption. Failure to establish strong data protection laws and ethical guidelines can lead to public distrust and reluctance in embracing AI technologies.

Regulatory Hurdles: Overly stringent or unclear regulatory frameworks can slow down AI innovation and adoption. Countries need to find a balance between regulating AI to ensure safety and ethics without stifling innovation. The EU and UK are leaning towards a more structured and holistic legal framework, while the US shows a more fragmented approach with some movement towards federal legislation. China's governance model, on the other hand, seems to be evolving in response to both internal and external factors, balancing innovation with societal control. All these strategies are shaping the AI world we live in, creating AI bubbles.

Public Perception and Resistance to Change: Resistance to technological change among the public and within organisations can slow down AI adoption. Misunderstandings and fears about AI, often stemming from a lack of awareness, can lead to resistance. The narrative is about the negative, the risk to jobs, rather than the value added and the opportunities AI and generative AI can deliver. Perception matters as it leads to trust. Reputation matters.

Global Competition: The race for AI leadership is a global one. Intense competition from other countries, which may have more resources or a more aggressive approach, can undermine a nation's efforts to lead in AI. AI is everywhere, it crosses siloes, which is why those that are responsible for policy need to looks strategically and outside their usual boundaries.

Intellectual Property Challenges: Issues surrounding IP rights in AI can lead to legal battles and uncertainties, potentially slowing down innovation and collaboration in the field. The question here is, what data are the LLMs using to deliver generative AI solutions? is it open source data or copyrighted with IP? Are data owners rewarded for helping to build generative AI solutions?

Ethical and Societal Impacts: Concerns about the ethical implications of AI, such as job displacement, bias in AI algorithms, misinformation and the societal impact of autonomous systems, need to be addressed comprehensively.

Are the generative AI models that we are building for a global world or a Western world?

Ask yourself this question, who is building ChatGPT, Claude, Bard and all the other GPT and generative AI services? Where are they based? What is their primary language? What are their culture and societal norms?

Outside of the tech bubble, people live in communities, even hyperlocal environments where language accents and cultural norms help or hinder understanding.

Cultural issues play a significant role in how AI and generative AI learn and offer support, particularly concerning the diversity of written and spoken languages. These issues can impact the effectiveness, accessibility, and fairness of AI systems:

Language Bias in Training Data: Most AI models, especially generative ones, are trained on datasets predominantly in English or other major languages. This can lead to biases where the AI performs better in these languages and struggles with less common languages, potentially excluding non-English speakers or speakers of less common languages from fully benefiting from AI technologies.

Cultural Context and Nuances: Language is deeply intertwined with culture. AI models that lack exposure to diverse cultural contexts may misinterpret or misrepresent nuances, idioms, and cultural references. This can lead to misunderstandings or inappropriate responses, particularly in sensitive areas like mental health support or customer service.

Ethical and Societal Norms: Different cultures have varying ethical and societal norms, which can impact how AI is perceived and what is considered appropriate or acceptable in AI interactions. For instance, the directness of communication, notions of privacy, or the role of technology in decision-making can vary widely.

Localisation Challenges: Localising AI applications involves more than just translating language; it requires adapting the application to local customs, regulations, and user expectations. This can be a complex task, especially for generative AI models that need to understand and generate contextually appropriate content, but multilingual models that can handle 100+ languages are emerging to provide more global accessibility and applicability in various locales. That said, models optimized for single languages tend to show higher fidelity of generation. So diversity combined with specificity are both growing.

Representation in AI Development: The underrepresentation of certain cultures and languages in the AI field can lead to a lack of understanding and consideration of these perspectives in AI development. This can result in AI systems that do not fully cater to the needs of diverse global populations.

Accessibility Issues: The dominance of certain languages in AI can create accessibility barriers for non-native speakers or those with limited proficiency in these languages, thereby exacerbating digital divides.

Algorithmic Cultural Bias: AI algorithms can inadvertently learn and perpetuate cultural biases present in their training data, leading to unfair or biased decision-making processes that might disadvantage certain cultural groups.

To address these challenges, it is important for AI developers and researchers to focus on creating more inclusive and diverse datasets, incorporating multicultural and multilingual perspectives in AI development, and ensuring that AI systems are tested and adapted for different cultural contexts. Additionally, involving linguists, anthropologists, and other cultural experts in the AI development process can help in understanding and integrating cultural nuances more effectively.

We are living and working in an era where language is no longer just that; it is data, but when building generative AI tools, we need to consider local context to ensure the future we are building is for all and is safe.

We are in an era of change and opportunity. But also one of risk, where we need to be mindful of and ensure that perception and reputation matter if we are to see the return of value and growth from AI.

A recent study by PWC stated that AI innovations could contribute up to $15.7 trillion to the global economy by 2030! With the right ethical governance frameworks in place, generative AI may usher in a new era of inclusive and sustainable growth.

But before you see anywhere near these numbers, generative AI and other AI tools will require invest from, primarily, VCs, CVCs and others.

Make no mistake, for value and safety, companies will have to support their in-house or arms-length investment vehicles in order to identify how best they can find efficiency.

Venture capitalists have generally led the way in the past in supporting innovation, maybe, the time is now for corporate VCs.

The opportunities and value that generative AI can deliver need to be designed into the safety-net that citizens expect.

In an era of uncertanty, technology and innovation can deliver growth.

Open AI: How the Board turned an issue into a crisis

The Board of OpenAI created a crisis out of an internal issue. Their lack of focus or understanding of corporate governance led to not just the sacking of their CEO Sam Altman but their own departure after he returned to lead the company that he co-founded. All because of very poor communication. A lesson to learn for Boards and investors in start-ups everywhere

OpenAI CEO Sam Altman

Over the last weekend, in an act of corporate hara-kiri, OpenAI descended into chaos after its Board sacked founder Sam Altman.

The news shocked the technology sector, the wider stakeholders, and the general public, who, since it released Chat GPT-3 late last year, saw OpenAI as a leader and a model in Artificial intelligence. Sam Altman and OpenAI had taken AI and generative AI mainstream.

Its success caught many companies off guard, forcing them to enter a sector that could potentially disrupt many industry sectors.

OpenAI’s fundraising and company structure

OpenAI isn’t a new company. Founded in 2015 as a not-for-profit entity, the start-up has already gone through various issues, including an association with Elon Musk. The initial $1bn funding allowed it to have a path for growth and focus on ensuring ‘that safe artificial general intelligence is developed and benefits all of humanity.’

The immediate benefit was securing a $1bn investment from Microsoft to support its development of new technologies on Microsoft’s Azure cloud computing service and furthering OpenAI’s efforts in creating artificial general intelligence.

Increased investment forced Altman and OpenAI to establish a Board of Directors to give confidence to investors about it’s corporate governance processes. This is critical for any start-up, large or small, especially any that has the potential to scale at pace and burn through capital secured in order to grow and secure profit.

In July 2022, OpenAI raised $100 million in new funding from investors like Dustin Moskovitz's Valo Ventures and Jim Simons' Euclidean Capital. Fundraising and a $300 million share sale were made earlier in 2023, including Sequoia Capital, Andreessen Horowitz, Thrive and K2 Global, who put a valuation of the company at between $27bn – $29bn. Last month, in October, and six months since its last fundraising, OpenAI entered talks to sell further shares at a valuation of $86bn.

However, given the structure of the company, some changes would need to be made.

OpenAI would have also needed to consider making changes to the Board of the company in order to give investors more oversight and confidence, because until Altam was OpenAI had a Board of six people, three internal staff members and three external. Each of these brought specific skill sets to the table but lacked the necessary governance issues and risk management.

An issue I have discussed in the past is the lack of strategic communicators on the Boards of start-ups who can guide the company through issues that have the potential, reputationally or otherwise, to turn into crises.

The make-up of the Board and the advisers that a start-up has given markets, regulators and investors confidence and trust. It is essential for any company when they face critical challenges.

Up until Altman was fired, the board of OpenAI was formed by six people, three internal employees and three external. They all brought something to the table, but looking back, it looks like there was limited corporate governance and non-technical experience to help advise the C-suite on how to navigate any issues that they would face.

The growing stature of Sam Altman enabled him to attract investors and partners. His reputation and brand helped to grow the company, while the structure of his company was his Achillies heel.

And when the Board decided to fire Altman for reasons that they are yet to reveal, but focused on a lack of communication with them, well, their statement was guilty of the accusation they were making against Altman.

The Board of OpenAI found themselves in a bubble, without foresight of the reaction to their decision and how they communicated it.

Since Altman has left, we have learnt that::

Microsoft appears to have poached Altman and Brockman (Reuters)

The Board are not resigning or recognising their failure

Great reporting from the Pivot Podcast's Scott Galloway and Kara Swisher.

Where does this leave the OpenAI’s Board members?

Questions are now being asked about the six Board members of OpenAI. Ilya Sutskever, the last remaining co-founder on the Board, who was involved in the sacking, took to Twitter/X to apologise for his decision to sack Altman. He then signed the open letter asking other Board members members to quit.

As for the rest of the Board, Adam D’Angelo, chief executive of question-and-answer service Quora. Technology entrepreneurs Tasha McCauley and Helen Toner from the Center for Security and Emerging Technology at Georgetown University have damaged their reputations.

Their in-the-bubble behaviour has shown what the risk is of not keeping eyes on the C-suite or communicating effectively. It equally confirms that the Board of any start-up needs to be balanced. And yes, strategic counsel needs a seat on the table, and investors need to be engaged before any such decision is made before any such decision is made public. And by the way, it appears that Microsoft’s CEO Satya Nadella only learnt about the decision after the trigger was pulled.

What can we learn from this corporate mess?

Sam Altman has created a whole new sector for technology that touches nearly all industry sectors. AI has the potential to transform any industry.

AI can help businesses evolve and secure additional value. This is thanks to data and the creation of personalisation and added enhanced experience.

Start-ups will come and go. Some with hype, but many will be bought out and integrated into an enterprise stack, so for the growth of any AI business, what they need to know more about is that reputations and trust matter, during their fundraising, during their growth and when they will be required to give oversight to regulators.

Additionally, Boards need to be balanced. They need experience and have the ability to not just have technical knowledge, but also corporate and reputational governance.

Venture Capital (VC), Corporate Venture Capital (CVC) and Private Equity firms will require a team that is on board, and that can guide a start-up to growth stages and beyond that can, manage and mitigate any risk and effectively advise the company’s leadership, as well as investors.

The days of a start-up marking their own work and thinking that reputation doesn’t impact growth are gone, yet.

How the cult of personality and tech-bro culture is killing technology

You might have noticed that the digital and tech worlds are going through turbulent times. All the recent headlines have been around the chaos of Twitter since the takeover by Elon Musk, Mark Zuckerberg's spending Meta’s billions on building his vision of the Metaverse, all while making over 10,000 people redundant, and a certain Sam Bankman-Fried, who has tanked FTX because of, well, just having no management processes in place. Needless to say, he has confirmed to many the suspicions of the crypto world.

Every piece of damage in each of these evolving stories is very much self-inflicted, and it’s been allowed to happen because of both the tech-bro culture and cult of the personality that has been allowed to go unchecked by funders for far too long.

Sadly, toxic and extreme working cultures are not new. Just look at the financial and political worlds. What we’ve seen in tech is a growing acceptance that to achieve growth and a healthy return on investment, and equally, to not miss out on the next best thing, you have to be committed to a hardcore culture,’ as Elon Musk recently said.

But the three companies that I mention are not the exception, and there are many more. Just look at Uber under Travis Kalanick in the early days or WeWork under Adam Neumann.

Strong alpha leaders have been, if not encouraged, then certainly accepted. And it is these leaders who are nurtured and grown and use their profiles to scale their businesses. It is not just the product that people invest in, but the personality.

When a start-up grows, they have a story to tell. At this early stage, communications support tends to be limited, and whatever counsel is there is focused on promotion rather than protection. It’s all about scaling the business and tightly so meeting the expectations of investors. BUT, it is here where investors need to focus more extra time on the character and behaviour of the founder/s, and if they are going to pose a risk to not just the business they are trying to grow but to the investors themselves.

Pre-IPO, due diligence on risk and reputation is an internal matter. Funders will look at it from the perspective of the balance sheet, especially against their other projects. But, aside from the expertise, what is often needed is a handler that is established by a funder to ensure that a start-up can deliver and do so in a manner that protects not just the investment made but the reputation of the investor and the wider sector.

Look at the situation of FTX. It was a great story with a great narrative, something that secured a great investment and valuation, but equally a story that created a distraction that even now is unravelling in such a way that established many questions about not just how the exchange was run, but the due-diligence processes that investors had in place.

And talking about due diligence, the recent Theranos story is a great example, where the profile of Elizabeth Holmes was carefully crafted and sold to the media and, by default, to other investors. A person that appeared not to be part of the tech-bro crowd but was just this week convicted of defrauding investors.

And Elon Musk, who, after his dance with Twitter, finally bought the company with the help of additional investors. All before, very publicly, doing everything to damage the business model that is over-reliant on advertising.

With Twitter, it is no longer about due-diligence, but about him and his view and his own view or what and how he wants to remake a business that cost him $44 billion dollars, regardless of the fact that others have investment in him and Twitter.

Technology has not yet reached peaked. What it has reached though is a point where investors, even SoftBank, are looking to minimise their exposure to investing on a hunch and where reputation and culture can be brushed aside as a minor issue.

Reputation, risk and due diligence are essential areas that investors might spend a bit more time on to limit their exposure to stories that might be too good to be true.

Elon’s Twitter Problem

Is the bird free?

Elon is the new owner of Twitter, and since the deal was finally completed last week, he’s wasted no time in getting involved in every detail area of the company. He’s focused on doing things his way. Let’s be clear, it is now his company and toy, and he can do whatever he wants with it. But, to buy the company, he’s had to use not just his money but that from partners and banks, and that creates a huge problem for him.

So, let’s unpick some of the issues that Elon has created for himself. They are anything, from the issues relating to the quality of the product and experience to its over-reliance on advertising in its generation of revenue. And let’s not forget about the toxicity of some of the users, who hide behind anonymous accounts to troll, dox and spread hate speech.

All that said, does Twitter have the potential to become something greater than it currently is? Yes, but that will mean Elon stepping out of his bubble and looking and what works and what doesn’t in real life.

So, the issues …

Funders

To complete the deal, Elon has had to use the equity he has together with additional debt financing from lenders to cover the cost of the deal.

It is reported that $13 billion of debt will be financed by banks, who only this week said that they are preparing to keep $12.7bn Twitter debt on their books until early 2023, which could lead them to incur huge losses. That is already bad for the bank, but with the debt and the rise of borrowing, Twitter is now likely to pay ‘roughly $1 billion a year in annual interest payments — more than Twitter’s total profits for 2021.’ Just think about that annual interest payment before anything else to keep the firm afloat!

All this, together with the fact that banks are yet to see a clear strategy, creates a challenging situation for Elon, who has put himself front and centre in owning the company and turning it around.

To make it into his global town square, Elon is going to need a lot more money than he thought he did, which is going to be difficult. After all, unlike with Tesla and SpaceX, here he is selling a service, a channel of communications with limited experience for the end users just yet!

Advertisers

One of the biggest issues for social media companies is their addiction to advertising money. For many, Meta included, their revenue streams come exclusively from the income they generate from advertising.

According to estimates from eMarketer, in the US alone, advertisers ‘are on track to spend $65.3bn on networks such as Facebook, Snap and Twitter this year, a year-on-year increase of just 3.6 per cent.’ All that sounds good, but it is ten times slower than in 2021. Yes, a lot of money, but there is a downward trend in this service spending as businesses are looking at better returns from their investment. Advertisers are refocusing on where they put the money they use to reach their audiences.

Those that know me to know that I am suspected of advertising on digital and social channels. I have always found the metrics they use to highlight success to be shocking. Engagement on Instagram of two or three percent and people celebrate. Yeah, but what about the 95% of the spent money? Yeah, exactly.

So in this situation what does Elon Musk do? He decides to restructure Twitter into an entity that establishes the perception that there is a rise in hate speech on a platform where businesses spend their valued advertising money.

Advertising income for Twitter is nearly their exclusive revenue stream, so rather than engage them and keep them onboard while he redesigns the firm, he opts to make them nervous. The money reacts with many now opting to money their spend elsewhere, to which Elon then write a grovelling Tweet.

As Scott Galloway points out, ‘advertisers have a choice.’ Advertisers are opting for stability. They are not signing up to his view of what a communications ecosystem should be with limited moderation.

Elon is making the restructuring of Twitter even harder because he is trying to please too many audiences.

And while he maintains his belief of freedom of speech, he is failing to realise that the world has physical and cultural borders and Twitter is a global company.

Staff

Just recently, Elon announced in no uncertain terms that he’s going to be trimming down the size of the workforce, most probably to satisfy the requirements of the lenders that have helped him buy the company. Oh, and the fact, maybe, that revenue from advertising is dropping.

Numbers being leaked range from a reduction in the workforce from 50-70% worldwide. Crazy numbers.

Staff have already received emails telling them not to turn up to work, and USA class-action lawsuits are already being filed in California against this mass firing.

Regulators

Yes, the law. We know Elon’s view on regulators. He and the SEC have form, and to a certain extent, that was a modest situation compared to what might be coming his way given what’s at stake with Twitter and the influence of the platform.

The EU has eyes on him, as does the US, specifically on national security matters given that the channels was bought with foreign investors.

It was reported by the Washington Post that “terms of the deal give large foreign investors access to confidential information about the social media platform.”

Haters

The platform is changing. As much control as Musk has, there needs to be a realisation that the platform is where it is because of the lack of innovation that took place and the decision not to focus the platform on relying solely on advertising revenue.

Twitter has not done as much as it could have to manage the discourse that takes place on the platform. Yes, it has moderation tools, but it has failed to see that the platform is accessed across international jurisdictions, where Elon’s definition of free speech is different.

Misinformation and hate continue to spread and such content has increased since Elon took the platform private.

A report by Forbes suggested that content moderation tools were being limited, highlighting the gap that exists between Elon and current and prospective funders. The question now is if Elon will realise that the opinions of businesses matter.

Super App

Elon is onto something here with turning Twitter into a super-App like the ones that exist in Asia, such as Grab, Go-Jek, WeChat and AliPay. These Apps have been designed as a gateway for conversation and commerce, and they work.

Dwell time in these apps is high as they deliver anything that you generally want. As a result, they capture a lot of data on your activity that is used ti keep you further engaged and deliver other services relevant to your behaviour.

The thing here is that the super-App started in Asia, and now you have Elon, who is trying to do something that Meta has not been able to achieve.

Even if it does achieve this and so brings in new users, who spend more time on the platform and money through it, it will not be innovative, an issue that Twitter is facing.

What he has to realise is that he needs to separate his views from the reality of running his past companies.

Having a global town sounds great, but in every town square, there are things that are moderated.

Twitter is a global tool, and Elon needs to realise this in how he and his team aim to redesign it, especially if he wants to avoid any issues.

Three issues that Elon Musk must fix as the new owner of Twitter

Elon Musk has bought Twitter, the de-facto channel used by government, politicians and media organisations from around the world to engage with and listen to the public. This purchase is not about freedom of speech, it is about control and shaping policy around the world.

After two weeks of flirting, Twitter announced that it had accepted Elon Musk’s $44 billion offer to buy the company and take it back into private ownership.

The news came as a shock, as many were initially doubtful that he could come up with the money to seal the deal. But that is what he did. Musk worked with Morgan Stanley to create a $25.5 billion debt financing plan before committing his own funds and equity.

What happens next is anyone's guess. But from what he’s publicly said, we know that there will be change at the company and some people are jubelous about this.

What we do know is that Elon is a staunch libertarian and a free speech absolutist.

In comments he’s made on Twitter as well as at past events that he has spoken at, Elon has made it clear that he did not support the content moderation policies and protocols that the company had put in place.

So, in all, the narrative is simple, the purchase of Twitter by Elon Musk is all about free speech. It is not, at least for now, about the economics. He’s even insinuated that he would do away with advertising as a revenue source.

So what is Musk getting for the money that he is investing in the firm? Well, one thing is certain, he is getting a company with potential, but even greater risks and issues that to date many fof the current team have been unable to resolve.

Elon is getting a company with a great concept, that has not maximised it’s potential by far, but which has gathered onto it’s platform the good and the great from an wide array of sectors including politics, governments and media, as well as entertainment and others who influencers the millions of passive users.

Just look at how many politicians and government departments from around the world take to Twitter to announce a new policy?

Think about it, the days of issuing a press release to share your policy and views to the media and their audiences are long gone. He is now the owner of the channel through which people can share their feedback on policy and politics. Or at least feedback from those who decide to engage, let’s call them the vocal minority.

For Musk, owning Twitter is about influencing not just opinion, but also policy and behaviour in the US and around the world.

While Jeff Bezos and Rupert Murdoch own traditional media outlets, Elon has gone in full digital and bought the channel that their media outlets and journalists promote their stories and content on. He has not just bought the ticker-tape, but the room in which people discuss the news, which is why how Twitter develops and iterates under his stewardship could have a profound effect and impact on how democracies function.

Let me be clear though, the buy-out comes with a huge risks for everyone. Let’s break these risks down.

Firstly, Twitter’s user base, which currently has 436 million active users, it is small and currently stands 15th most active social media platform worldwide. Compare that to Meta, which with it’s Facebook and Instagram apps, has a reach of 2.9bn monthly users.

In the US, Twitter has a reach of c.76 million users (27.3%) of the population, compared to Japan with 58 million (52%), Brazil with 19 million (10%), the UK with 18 million (31%), Indonesia with 18 million (8%) or Saudia Arabia with 14 million (50%).

Twitter has been struggling to grow its user base globally and to help it become the de-facto town square that Elon sees it as, which is why it is going to need to work miracles in order to grow to the level that it can compete with Facebook for audience base and it being representative of each nation.

Elon is going to have to get Twitter to really innovate. It is going to have to pump a lot of extra money in and change the culture so that innovation delivers value, both societal and eventually financial. This kind of business will eventually need to pay for itself.

And no, lifting restrictions on banned people is not going to help, because while influencers might return, many of the audience and users could leave, making it into an echo chamber.

Secondly. Let’s look at the issues surrounding the content on the platform and how you can make it a platform where people want to be without the hate, trolling and threats.

Elon states that all this is about ‘freedom of speech’, but he needs to remember that there isn’t one definition of free speech unless he thinks that his interpretation is the only one that counts.

Elon is talking about freedom of speech from the perspective of the US Constitution’s First Amendment, which is only relevant to audiences in the US. Unless that is he is trying to export their US Constitutional interpretation around the world and if he is then he is in for a major problem with that given the fact that 1) most users of Twitter are live outside of the US, and 2) while Twitter can generally be accessed anywhere, each other country and legal jurisdiction has its own interpretation of what free speech is, because with freedom of speech comes responsibilities, which he appears to be ignoring.

The EU’s commissioner for the internal market Thierry Breton has said that Twitter must follow rules on moderating illegal and harmful content online, saying, “Anyone who wants to benefit from this market will have to fulfil our rules.” Before adding. “If [Twitter] does not comply with our law, there are sanctions — 6 per cent of the revenue and, if they continue, banned from operating in Europe.”

Like other US digital and social media companies, Twitter is protected by Section 230 of the US Communications Decency Act, which states that “interactive computer service” can’t be treated as the publisher or speaker of third-party content.

Under this protection, if a user on Twitter publishes something libellous, the company holds no responsibility and legal mitigation can only be brought against the individual, rather than against the company as it is not seen as the publisher of such content.

In such situations, if a UK recipient of a libel claim wanted to recourse to legal action, they would need to take it both in UK courts and if necessary in US state or federal court to get the content removed. But this only works if you know the individual who has published the content, or even the bots that have amplified it.

The issue of users not needing to verify their identity is a critical issue in how Twitter [and Facebook and others social media companies] operate. Through the veil of anonymity, users can publish anything with minimum risk against them, highlighting what a town square is.

Elon is going to have to face this, bearing in mind that users have been conditioned to not share their official ID to access and use the service.

Thirdly, the service and the experience that users get. Twitter is great at one thing and one thing only. But it does not innovate or offer iterations that have made the service more relevant.

Look for example at the rise of TikTok or Instagram, or Reels. Twitter has tried to innovate, but it has failed and failed badly.

What you now see is people using multiple platforms for the content, from Twitter, Facebook, Instagram to WhatsApp and Youtube. Meta is the only company that has tried to keep the experience under one roof.

So yes, Twitter is a great product and service, but this purchase is not about freedom of speech or giving you a platform. This is about power and control and how we are now as a society moving into an era where those on social media can influence how governments and the corporate world shapes and implement policies.

But to do that it is going to have to make the town square even and a safe space for everyone, where you know who everyone is and where you can say your piece without fear.

Elon is going to also ensure that facts matter and misinformation and disinformation campaigns do not take place on his platform. After all, just days ago former US President Barack Obama gave a speech at Stanford University to raise awareness of how online misinformation and disinformation campaigns and content threaten the foundations of democracy.

Elon has bought himself a huge challenge!

Growing the reputation of Corporate Venture Capital

Corporate Venture Capital (CVC) firms are serious investors. Yet while venture capital (VC) firms get the headlines, CVCs can offer insight and industry-specific expertise that can help start-ups they support scale. Yet, CVCs and the value they can share are not as well known.

Look at your phone, at the apps that you have downloaded and regularly use. The chances are that these apps all started thanks to venture capital (VC) investment. Somebody had an idea for a service, a business. But to make it happen what they needed is money.

Venture capitalists are the ones who get the headlines, who take the risk and in return for equity invest money that turn ideas into reality. VCs like Sequoia, Andreessen Horowitz, Kleiner Perkins, Accel and many others fuel innovation that help disruptive concepts become the likes of Facebook, Airbnb, Alibaba, Okta and Github and so many more.

But VCs are not the only source of money in the market, and for many start-ups a VC might not be the best partner either as there is a clear difference between what VCs want in return for equity and what corporate venture capital (CVC) want and can equally offer as part of the deal to make a business happen.

Searches for VCs vs. CVCs

What is Corporate Venture Capital?

CVCs are investment vehicles created and owned by enterprise organisations through which they can invest capital and knowledge directly into start-ups in return for equity.

Like VCs, CVCs invest if they see growth potential, i.e. generate a profitable return in the medium to long-term. For CVCs the return they are after might not just be financial, what they could be looking for is technology that add value to their parent company and the way in which they operates. Equally, having control of intellectual property that can help their business grow.

For corporates enterprises that invest, CVCs can play a very strategic part in safeguarding their future and growth opportunities.

In return for equity, investment from a corporate can include knowledge and expertise that can help a start-up scale and come online.

Just look at the health sector and how CVCs from firms like Pfizer, Johnson & Johnson and many others are investing in health and med-tech opportunities as we move from the COVID-19 pandemic to a state of endemic. The last two years has created an appetite for an improvement in healthcare that can be delivered through bio-tech, digital therapeutics, health IT, mental health and wellness, and telehealth.

A record year for CVC deals

What are the challenges facing CVC firms?

At a recent Global Corporate Venturing webinar a discussion took place not just about the deals that took place in 2021, but also about the challenges that surprisingly CVC still face.

CVCs have two primary challenges, which relate to:

How they are perceived within their parent companies, and

The awareness, or lack of, amongst start-ups regarding what they can also offer aside from capital.

Some great data was presented during the webinar, including a recent research paper by Ilya Strebulaev, a professor of finance at Stanford Graduate School of Business, and research fellow Amanda Wang, a key finding was ‘a general lack of knowledge about venture capital among corporate leadership.’

The research, which took place over nine months and interviewed senior investment professionals working in the VC units of 74 U.S. companies (representing almost 80% of all CVC units in the S&P 500) found that more than 60% of senior executives confided that their parent companies do not understand the norms of venture capital. Something that shocked me!

Enterprise CVC units were often kept at arms-length, with no two corporate venture capital units being alike, an issue not just for reporting and transparency, but one that slowed down the ability of CVCs to compete to get the deal done.

Some CVCs also stated anonymously that there was often not a clear sense of objectives set, with the investment numbers being presented just as an R&D expense. Against, value added and risk management were not often identified for parent companies.

Yes, like VCs, CVCs will have an exit strategy for their investments, but more often than not and with the right strategic aspirations and internal culture within their parent company, CVCs can also be more forward looking and help the parent company better manage competitive risk. Again, if the company thinks long-term and understands the value that their CVC can offer them.

Some outcomes for a parent company’s CVC strategy can include integration of new technology solutions into supply chain, ownership of IP, better positioning and market capture.

How can communications help CVCs?

Communications is an essential tool in order to better position the value that CVCs provide to both the parent company and the organisation that is seeking investment in order to grow and expand.

The GSB study shows that work is needed to map stakeholders and raise awareness amongst them of the work and value that CVCs provide to their parent companies.

Stakeholder mapping, engagement and management require insight and time in order to secure a better understanding of the value that they can add.

At the same time, a strong communications operation is needed in order to highlight the deals that CVCs are securing, because at the moment it is VCs that are getting the headlines, at least in the tech environment.

Each parent company will have their own objectives, set on the benefits and returns that they want from their CVC, and if they do not have these then work is needed to help establish these.

Messaging, storytelling and reputation management are critical areas of work that are needed. Equally, when an investment is made these are also essential knowledge areas that need to be leveraged within the organisations that they have invested in. The reputation of a start-up needs to be carefully developed and managed during the early stages of scaling. Reputation matters when you are looking to create trust. It really is about identifying risk and establishing confidence, not just in the company, but also in the founders.

The perception of innovation can increase teh reputation of many companies, which is why CVCs through their investments can also support the setting of this perception. This is something that is more of a long-term outcome of an effective strategic communciations policy, but one that over time will also help attract future investments as start-ups and founders decide who is better placed to help turn their disruptive ideas into a reality.

Look at the video conferencing app Zoom, which grew during the pandemic. In April last year, it launched a $100 million fund through which it plans to invest in businesses that are developing solutions that Zoom feel can add value to its own operations.

Zoom reported earnings of $2.65 billion, an increase of over 320% compared to the previous year. And with a focus on hybrid and remote working, the space is there to establish this business in the work ecosystem, making an investment vehicle a logical solution. By the end of 2021 Zoom had invested in more than 25 Apps.

Some of these Apps might be integrated into their environment, others might be sold.

There has been an increase in deals and investment in the past two years, with companies in the health, IT and media sectors receiving the largest investments from CVCs.

The time has come to establish communications as a key discipline in the CVC armoury to help it secure the recognition that it deserves, better manage the risk and reputation of its investments and better position it with its wide array of stakeholders.

This is not just about storytelling, it is about reputation management!