Corporate Venture Capital: The Human Innovation Gap

GCV Founder James Mawson at GCV Symposium 2026

I spent two days this week at the Global Corporate Venturing Symposium in London. GCV is one of the most concentrated rooms in the world for corporate venture capital, bringing together investors and fund managers, strategists, innovators and frontier technology founders, government advisers and more. All from across the corporate ecosystem. All gathering to take stock of where capital is moving and why, and the blockers and opportunities that exist.

I attend as a delegate and as an adviser. I have been part of this community since it was founded. And I will say this clearly: the 2026 edition felt different. Not because of the data, though the numbers were striking. It felt different because of what was unsaid, and what was said too quietly.

The pace of innovation is fast. But it is us, humans, that are limiting the pace at which much of this can be commercialised.

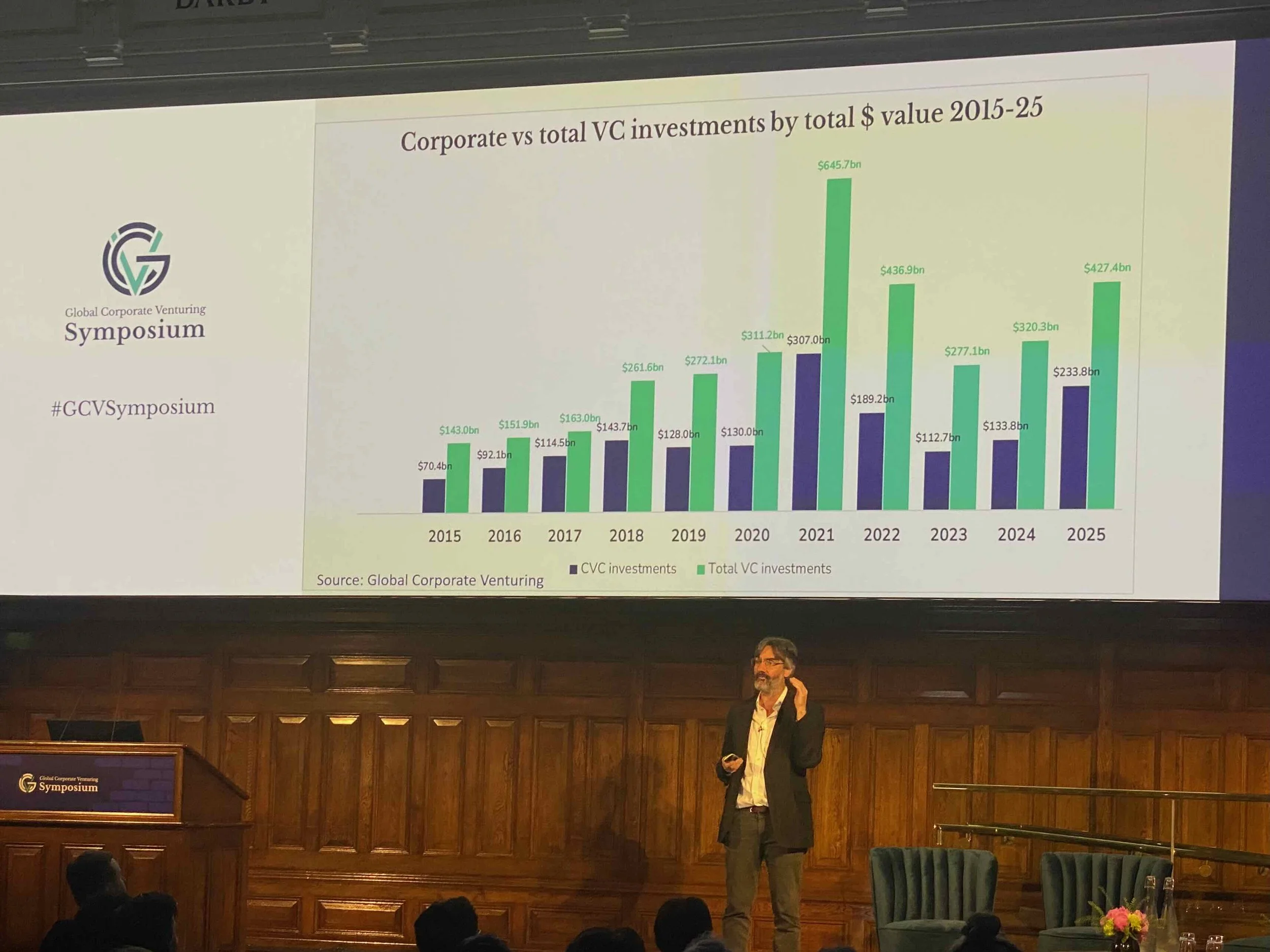

First, the context

GCV has been tracking the corporate venture capital ecosystem for more than fifteen years. The organisation publishes analysis, runs the global data, and convenes the community across cities from London to San Francisco, Tokyo to São Paulo. Its annual symposium is the clearest signal of where the sector's thinking is at any given moment. The events in Monterey in California, as well as in Tokyo give you a picture of where the opportunities exist in North America as well as in Japan and the rest of Asia.

This year, that thinking was shaped by three forces operating simultaneously in a way that has not happened before. Jim Mawson, GCV's founder, opened symposium by naming them:

A financial cycle running near historic highs in both equity and debt markets,

A technology cycle accelerating from software into the physical world, and

A geopolitical cycle reshaping the terms on which capital, talent, and technology can move across borders.

None of these is new in isolation. Together, they are creating a qualitatively different environment. The implication is that decisions made in the next two to three years, by investors, by corporations, and by governments, will have consequences that last decades.

The data gives that framing some weight. CVC investments generated approximately $55 billion in financial returns against parent company net income in the first quarter of this year alone. Exits across corporate-backed ventures reached a record $258 billion in a single month. The global venture ecosystem has grown from around $60 billion in 2010 to more than $600 billion at peak, and corporations have not only stayed in through the recent pullback, they have increased their proportional share of involvement.

And yet, across nearly every session I attended, the conversation kept returning to the same obstruction. Not a technical failure. Not a capital shortage, at least not structurally. As I said at the start, a human problem.

The real bottleneck: culture and risk aversion

I will be direct about what I heard others share.

In the defence and dual-use innovation roundtable, which was held under Chatham House rules and included investors and people with direct operational experience from the front line in Ukraine, corporate investors with decades in the energy sector, investors from Japan, Canada, and Germany, and representatives from some of Europe's largest defence primes. The conversation was frank.

What emerged was a clear and uncomfortable consensus: commercial technology is outpacing government-procured defence capability by a significant and widening margin. The reason is not a lack of innovation. The reason is procurement culture that is outdated and risk-averse.

One participant, speaking from direct military experience, described the current attrition dynamics in Ukraine: autonomous systems deployed at scale, kill chains compressed to seconds, iteration cycles measured in weeks rather than years. They returned to the UK and found government structures that could not contemplate this pace. Their conclusion as that of others round the table was blunt: a professional Western army would be destroyed at current attrition rates before government procurement cycles could respond to the threat.

This is not a hypothetical. It is a structural institutional failure.

The UK government's own Strategic Defence Review, published in 2025, called for innovation at ‘wartime pace’ and for ‘root and branch’ reform of MOD procurement. The SDR highlighted a persistent reality: the MoD tends to buy well-defined programmes from established primes, rather than investing in early-stage innovation or allowing new technologies to evolve through partnership with scaleups. The Defence Industrial Strategy followed in September 2025, creating a new UK Defence Innovation unit with a ring-fenced budget of £400 million. Yet procurement reform, framed in the Review as a break from 'business as usual', has yet to generate visible change.

And let's not forget the tensions that finally broke into the open in the UK. The chronic standoff between the MoD and the Treasury over the long-delayed Defence Investment Plan (DIP) reached breaking point on 11 June 2026, when the then Secretary of State for Defence John Healey resigned, writing to the Prime Minister that the Treasury had been "unwilling to commit the resources that the nation needs," and that the proposed DIP settlement would force him to "make decisions that would reduce the readiness of our Forces and increase the risk to personnel on operations, and could make the country less safe." The settlement he received reportedly fell £6 billion short of what he had sought, with the Treasury refusing to move beyond £12 billion against Healey's request for £18 billion. Minister Luke Pollard, who now holds responsibility for defence readiness and industry, has publicly called for faster procurement and promised to cut contracting times, stating at DPRTE 2026 that the aim is to remove "rules that get in the way of delivering the capabilities that our Forces need at a faster pace." The ambition is right. But the resignation of a defence secretary over a funding gap that everybody in the room at GCV already knew existed suggests the gap between stated intent and institutional will remains very wide indeed.

The fact is that the gap between what is stated and what is delivered is itself a trust problem. Companies and investors read the signals, calibrate their expectations, and then encounter the reality. The credibility of the system suffers, and so does the pipeline of innovation.

This is not unique to defence. Across other sessions, which covered robotics, physical AI, blockchain infrastructure, and space, the pattern repeated. What we heard was that the technology was ready and the investment appetite was there. The blocker though was internal culture: the risk aversion of procurement officers, the resistance of legacy approval processes, the instinct of large organisations to protect existing capability rather than cannibalise it for something better.

In the physical AI session, one observation that was made stayed with me. It was about the framing around robotics deployment in public environments. The question was not whether the technology worked. It was whether any company wanted to be responsible for the first visible failure in a public setting, because the reputational and regulatory consequences would set the entire sector back by years. That is a rational calculation. It is also a collective action problem that no single company can solve alone. And it is, at its root, a culture problem disguised as a risk management problem.

The European capital gap is real, and it has a perception dimension

GCV brought together leaders in European innovation policy, including a keynote from the European Investment Fund and a conversation with the European Innovation Council, both of which were instructive.

Europe's structural challenge is well known: excellent research infrastructure, deep industrial capability, a genuine talent base, and a persistent failure to provide growth capital at the stage where companies most need it. The question that was asked at GCV is no longer whether Europe can create great companies. It is whether it can keep them.

The European Champions Initiative, now entering its second phase, has catalysed fifteen funds capable of raising EUR 1 billion or more, with forty-five portfolio companies and eleven unicorns already emerging from the programme. That is real progress. But the exit problem remains: European companies continue to seek US listings because European secondary markets lack the depth to absorb them at scale.

What struck me about this session was the explicit reframing of what corporate investors are now expected to be. The language was precise: no longer participants in the ecosystem, but system shapers. The value proposition expected of corporate capital is not just the cheque. It is the supply chain access, the customer relationships, the regulatory credibility, and the ability to scale an innovation across a value chain in ways a financial investor simply cannot.

This is, if taken seriously, a significant expansion of responsibility. And it requires a different kind of internal culture within corporates, one that can tolerate the ambiguity of early-stage partnership without demanding the certainty of a procurement contract.

China is not resting

I want to name something that hovered over the geopolitical conversation without always being stated directly.

China's pace of innovation in technology areas that were supposed to be constrained by Western export controls is accelerating, not slowing. Chinese AI developers have increasingly optimised their models to run on homegrown hardware, rather than Nvidia's widely used CUDA ecosystem. Goldman Sachs analysts noted in May that they believe the pivot to domestic chips will accelerate over 2026 to 2028, pointing out that DeepSeek V4 works with eight China-made chips, including those from Huawei and Alibaba.

More strikingly, this week came news that Chinese AI startup Z.ai's flagship GLM-5.2 model, released shortly after Anthropic disabled worldwide access to its most advanced models, stunned global users after its performance benchmarks narrowly trailed leading closed-source models. GLM-5.2 now holds fourth place on Artificial Analysis' LLM intelligence leaderboard and operates at roughly a sixth of the cost of closed US frontier models.

The sudden withdrawal of closed US frontier models unleashed severe anxiety among global allies such as Canada and France, whose leaders heavily criticised over-reliance on US-controlled AI infrastructure at a G7 summit last week.

The pattern is consistent and important: where Western export controls and access restrictions create a gap, Chinese companies fill it, and they fill it faster than Western observers expect. This is not malign. It is rational. Constraint is a forcing function for innovation. The Chinese experience of building without Nvidia, of developing AI models despite semiconductor restrictions, of scaling autonomous vehicle fleets because regulatory environments were more permissive, is producing engineering capability and operational data that no amount of benchmark comparisons can fully capture.

One figure shared in the GCV defence session is worth sitting with: China currently has approximately two hundred robotics companies preparing for IPO. The comparable figure for the West is significantly smaller. This is not about threat framing. It is about the pace differential, and what it means for where the capability advantage sits in ten years.

In life sciences, a parallel dynamic is visible. Chinese pharmaceutical and biotech companies, facing domestic regulatory environments that in some areas move faster than Western equivalents, have used that speed to accumulate clinical data and manufacturing scale that is now genuinely competitive at the global frontier.

The lesson here is not that constraints are desirable. It is that cultures that treat constraints as problems to solve, rather than reasons to delay, generate outcomes that cultures oriented around risk avoidance do not.

Space: sovereign anxiety meets commercial opportunity

The space session was, for me, one of the most clarifying of the event. The commercial space market reached $614 billion in value last year, roughly twice the size of the AI market in the same period. Investment into space startups in the twelve months to end of Q1 2026 reached $18.8 billion, against $1 billion a decade ago when the first space-focused venture fund was launched.

But the conversation that mattered most was about sovereignty and dependency. The exposure created by reliance on a single commercial provider for communications infrastructure in a conflict zone has concentrated minds across governments. The question being asked is no longer whether sovereign space capability matters. It is how to build and finance it without creating the same dependency in a different form.

The most useful framing offered in the session was this: sovereign capital should be a signal, not a solution. Government investment validates markets and can crowd in private capital. It cannot substitute for commercial viability. The companies that thrive in the next phase will be those that can serve multiple national customers across different regulatory environments without being captured by any single government's agenda.

That is a strategic communications and trust problem as much as a technical one.

Blockchain and stablecoins: the infrastructure story nobody is telling well

The blockchain session was moderated by the Sony Innovation Fund and featured companies operating at opposite ends of the maturity spectrum: institutional crypto trading infrastructure, stablecoin payments across Africa and Latin America, and Japanese entertainment culture on-chain.

The most significant observation came from the stablecoin discussion. An average remittance transaction currently involves seven separate companies between sender and receiver. Stablecoin rails eliminate the intermediary chain entirely. Banks in Africa, Latin America, and the Middle East are beginning to accept stablecoin remittances natively, crediting recipients in local currency without involving a payments company at any stage.

This is not a story about speculation. It is a story about infrastructure. And the reason it is not being told well is that the perception of blockchain, shaped by a decade of speculative excess, makes institutional and government audiences reflexively sceptical. The companies doing serious work in this space are managing a legacy reputation problem that has nothing to do with their current operations. That is a strategic communication challenge with significant commercial consequences.

My view

I have spent more than two decades working at the intersection of reputation, trust, and perception as strategic capital. What GCV 2026 confirmed for me is that these are no longer adjacent considerations to investment and innovation strategy. They are central to it.

The organisations that will win in the next decade are not the ones with the most capital, the most advanced technology, or the largest procurement budgets. They are the ones that can build internal cultures willing to accept the risk of moving faster than feels comfortable, that can manage the narrative around complex and sometimes threatening technologies in ways that build rather than destroy public and institutional trust, and that can work across the public-private boundary without being captured by either side.

The human problem is the strategy problem.

I see five things that matter now:

The triple cycle is real and it will not wait. The convergence of financial, technology, and geopolitical forces is no longer a talking point. It is a structural environment that requires decisions at a pace most organisations are not yet culturally equipped to match.

Internal sponsorship determines external outcomes. In every corporate context at GCV, from a GCC bank building its CVC function to a European industrial company embedding AI into capital project management, the pattern was identical: the investments that succeeded had a strong internal champion. The ones that stalled did not. This is a culture question before it is a strategy question.

Procurement reform is a perception problem as much as a process problem. The UK's stated ambition to procure at ‘wartime pace’ is the right framing. The gap between that framing and current practice is where trust is being lost, with innovators, with investors, and with allies. Procurement processes need to evolve and iterate.

China's innovation culture deserves honest analysis, not reflexive framing. The pace at which Chinese companies have responded to supply chain constraints with engineering innovation is instructive. For all the challenges that Western markets have put in their way, they have learnt from these, evolved and adapted at pace. The lesson for Western organisations is not competitive anxiety. It is cultural: what happens when you treat a constraint as a design brief rather than a reason to wait?

Perception management is the rate-limiting factor. This was stated explicitly in the defence roundtable. I heard versions of it in every session. The technologies are ready. The capital is available. The blocker is human: the willingness to move, to accept visible risk, to manage the narrative in real time rather than after the fact.

Reputation is not what you say about yourself. It is what others believe about you, tested under conditions of stress.

Right now, the stress is real, and the test is underway.