Why Bond Markets Are Not the Enemy of Governments

LSEG Data

Imagine you are twenty-two, recently graduated, and you want to ask your parents for fifteen hundred pounds.

Version one. You walk into the kitchen and say: I need fifteen hundred pounds, can you help? There is a phone I want, and a holiday with friends, and I just need a bit of breathing room.

You already know what happens next. Your mother puts down whatever she is holding. Your father looks up. The questions begin. By the time the conversation is over, you are not getting the money, and the relationship has taken a small but real dent that will take a few Sunday lunches to repair.

Version two. Same kitchen, same parents, same fifteen hundred pounds. This time you say: I have found a short professional course that finishes in three months. Here is what it costs. Here is the role it qualifies me for. Here is how it will help me in my career, and here is the schedule on which I will pay you back.

The money is identical. The parents are identical. The conversation is not the same conversation at all. I’ve been there and chance are that we have all been there with our parents.

I have been thinking about this analogy for some time, because watching politics, statements, promises made by politicians often designed by their behind the scenes advisers make the first version of the request, in public, to audiences that behave almost exactly like parents. And then expressing surprise when the answer is no, or when the answer is yes but at a cost they did not expect to pay.

So, why am I raising this as an example? Well, for some time in the media we have been presented with statements about how the country and politicians are held hostage to the bond markets, a very interesting framing of them and us, the people.

The audiences are not adversaries

Bond markets are not villans. They are we the people. They are the aggregated judgement of millions of people who are trying to protect money that belongs to other people — future pensioners, policyholders, savers, sovereign wealth funds, pension trustees, regulators, foreign investors, and the editorial boards that shape how all of them think. They are not ideologically opposed to lending. They are simply trying to work out, from the words being used, whether the money is going somewhere that will enlarge the borrower's capacity to repay, or whether it is going somewhere that will simply meet a present want. In simple terms they want to understand the return on investment and over what time period.

That distinction, investment in future earning capacity versus consumption today, is, in the end, the only question that matters. It is the question your parents ask before they give you money. It is the question every credit committee asks before it signs. It is the question every bond market is asking right now of every government that wants to borrow at scale.

And it is the question that an astonishing amount of policy work, across the democratic world, is currently ignoring and not wanting to answer.

What the market is actually saying

It helps to look at what is happening in real time, because the numbers tell the story more clearly than the politics does.

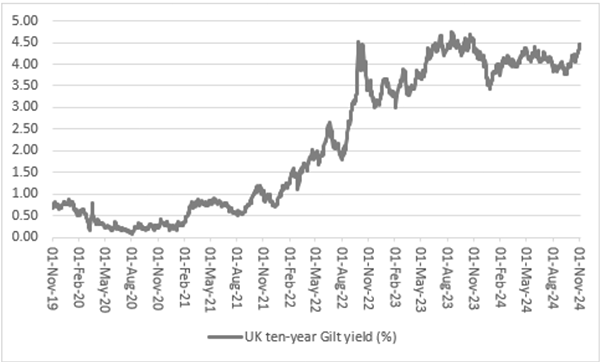

Today, the United Kingdom now has the highest government borrowing costs in the G7. The ten-year gilt is trading above five per cent, levels not seen since the financial crisis of 2008. The thirty-year, which is the better gauge of long-term confidence because that is where most sovereign debt is actually issued, has moved from around five per cent to nearly five and three-quarters per cent in three months. France is not far behind. Italy's spreads have widened. The United States is paying meaningfully more for ten-year money than it was eighteen months ago.

This is not unique to one country and it is not unique to one political party. It is happening, in different forms, in most advanced economies that are trying to borrow heavily at a moment when inflation has not yet fully retreated and growth is constrained.

But, and this is the part that gets lost in the daily commentary, the market is not refusing to lend. In April, the UK sold fifteen billion pounds of new ten-year gilts and drew a record one hundred and forty-eight billion pounds of orders. The investors are queuing up. They simply want to be paid more for the ‘trust’ they are being asked to extend, because the story they are being told about the borrowing does not yet add up to a credible account of how it will be repaid.

That is the parent test, performed in public, at the scale of a G7 economy.

Perception is not what happens after a policy. It is part of the policy.

Here is the part that the policy world keeps getting wrong or choosing to ignore because they might think it is easier to put a dead-cat on the table, and not just in one capital. There is a working assumption, embedded in think tanks, in policy units, in special adviser offices, in the briefing pipelines that feed political journalism, that the substance of a decision is one job and the communications of it are another job, and that the second job begins only when the first one ends.

It does not. The audience is forming its view of the substance through the framing. The two are the same act. A policy that cannot survive its own framing is not a finished policy. It is a draft.

Where this most often goes wrong is in the gap between two audiences that policy teams treat as if they were the same audience but plainly are not. There is the immediate audience, the voter who wants to know what is in this announcement for them this week, and there is the structural audience, the lender, the investor, the partner, the regulator, the next generation of taxpayers, who wants to know whether the announcement is part of a plan.

Too much current policy communication is optimised for the first audience and indifferent to the second. The result is announcements that read, even when they are dressed in the language of growth, as a series of disconnected promises to whichever constituency was loudest in the most recent week. The lender, listening from the trading floor of a pension fund in Toronto or a sovereign wealth office in the Gulf or Asia, hears no plan. Hearing no plan, the lender prices the absence of a plan, the risk and charges a risk-premium. And the absence of a plan is, in the end, what the rising yield curve is measuring.

The cost of being unable to tell a coherent story

The Institute for Fiscal Studies put a version of this point in its response to the most recent Spring Forecast: if spending plans are not viewed as deliverable, they will not be viewed as credible, and the wider fiscal package will be read accordingly. Credibility is not a separate property of a plan that can be added afterwards through better communications. It is one of the conditions a plan has to meet to count as a plan at all.

This is not about whether a government should support its citizens. That is the core remit of government. It is about whether the way that support is framed, and the way the borrowing that underwrites it is framed, describes a country that is enlarging its productive capacity, or a country that is distributing the proceeds of a productive capacity it has not yet built.

The same fiscal envelope can be presented as either. Consider two announcements that move the same amount of money:

We are going to borrow to support the people we represent.

That is the first version of the fifteen-hundred-pound request. It is not wrong. It is not even unpopular with the people being supported. It is simply unfinished, because it tells the lender nothing about return. The yield rises, the cost of every future ambition rises with it, and the constituencies the borrowing was meant to help end up with a smaller pot than they would have had under a better-framed version of exactly the same policy.

We are going to borrow to expand the productive capacity of the country. We are goingt to invest in increasing our energy capacity, imporoving our transport, simplifying ourplanning system, and we are going to do this so we can rebuild the country at pace so that the people we represent will be the first beneficiaries of the growth that follows.

Same money. Same constituencies. Different price.

Notice what has changed. The people the policy is intended to help are still there. They have not been abandoned, demoted, or rebranded as an inconvenience. They have been repositioned from the destination of the spending to the beneficiaries of what the spending produces. That repositioning is not spin. It is the difference between a story the market will pay to be part of and a story it will charge a premium to lend against.

Three questions every policy team should ask before announcing anything

The fix is unglamorous and entirely available. It is to put perception into the room while the policy is still being designed, not afterwards. Before anything is announced, three questions:

Who, specifically, is being asked to extend trust to this decision — voters, lenders, allies, investors, regulators, partners abroad? Each of those audiences is a separate parent in a separate kitchen, and they will not hear the same announcement the same way.

What story does the decision tell each of them about the kind of state they are dealing with? Is it the story of a country building something larger, or the story of a country distributing something already shrinking?

If the story is the wrong one for any of those audiences, is the answer to change the words, or to change the decision?

Most of the time, when policy teams work through these questions properly, they discover that the decision is broadly correct and the framing is wrong. Occasionally they discover the opposite, which is more uncomfortable but more valuable. Either way, the discipline pays for itself many times over in the cost of capital, the durability of political support, and the willingness of stakeholders to lean in rather than back away.

The work-life balance argument is the same argument

There is one more thing worth saying. The reason this matters beyond the bond market is that the absence of a credible plan does not only raise the cost of borrowing. It raises the cost of everything else.

It raises the cost of inward investment, because the investor cannot tell whether the regulatory regime will look the same in three years. It raises the cost of attracting talent, because the worker cannot tell whether the country is on a trajectory worth committing to. It raises the cost of partnership with allies, because the ally cannot tell whether the commitments being made today will survive the next reshuffle. And it raises the cost, quietly, of living — because a population that cannot see a plan cannot plan its own future around it, and a population that cannot plan its own future is a population that does not save, does not invest, and does not take the long view that growth ultimately depends on.

A credible plan, well framed, gives everyone, markets, allies, businesses, and citizens, the thing they need most in order to make their own long-term decisions. It is the single greatest gift a government can give the people it represents, and it costs almost nothing to provide, beyond the discipline of thinking properly about who is listening.

Reputation is strategic capital

There is a tendency, especially in technocratic circles, to treat perception, trust, and reputation as the soft edge of the policy world. The serious work is the spreadsheet. The communications come later, and someone else does them.

This is backwards and to me signals how little regard they have for people or understanding their own position, whether it is a voter or an investor. Reputation is strategic capital. It determines the rate at which a country can borrow, the speed at which it can attract investment, the willingness of allies to coordinate, and the patience of citizens when the dividends of a programme take longer to arrive than promised. Governments that understand this raise reputational capital deliberately, through the design of their decisions, not just through the language used to describe them. Governments that do not, spend it, often without realising they are doing so until the bill arrives in the form of higher yields, a thinner bid for new debt, or a coalition partner walking away.

The parents in the kitchen always had the fifteen hundred. The question was only ever whether you were going to ask for it in a way that made them want to give it to you and in a way in which they felt they were going to benefit from the investment they have been making in you to date.

That is the question every policy team, in every capital, ought to be putting at the front of the design process — not the back.