Why Now Is the Moment to Invest in UK Life Sciences Sector

Earlier today, I was invited by the UK Government's Office for Investment Venture Capital Unit to attend its Health Tech Showcase at The London Stock Exchange. The event brought together early-stage and growth-stage life sciences companies pitching to institutional investors, family offices, and sovereign capital. Ministers, sector CEOs, and global venture builders took the stage to make the case for the UK.

I left with a strong conviction, not just about the quality of the science in this country, but about the size of the story we are failing to tell.

This is that story.

The Numbers Are Better Than You Think

Let us start with the data, because the data is remarkable and it is not making enough noise.

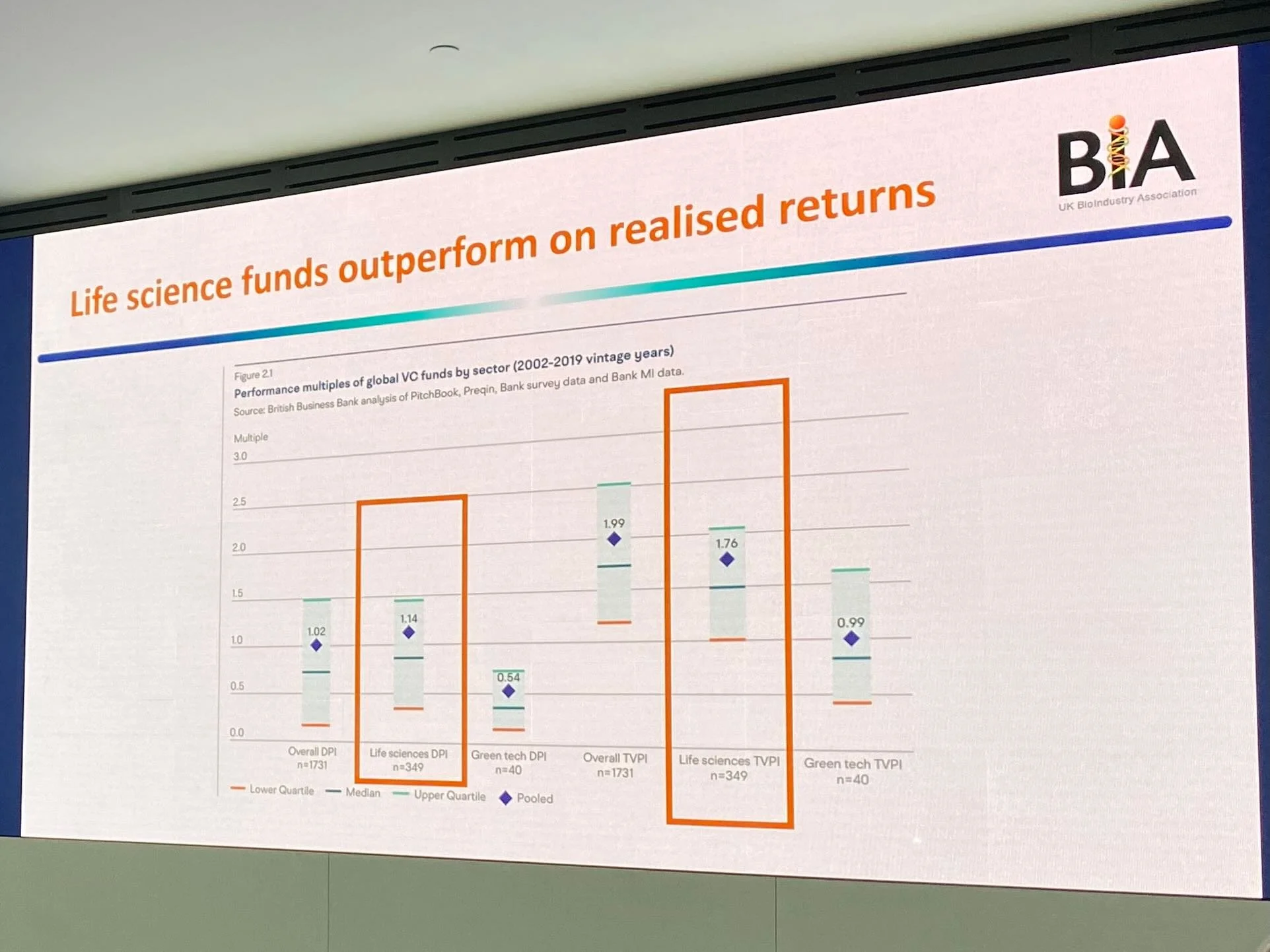

The UK listed life sciences sector is valued at approximately £400 billion. Around 320 companies span the London market, from micro-cap biotechs to global pharmaceutical groups. Venture capital investment in UK life sciences closed 2025 at £3.37 billion. That figure represented a 12% moderation from the prior year, but it still outperforms long-term historical averages and signals sustained structural confidence in the UK's scientific base.

In London specifically, companies leveraging AI secured more than half of all life sciences investment raised so far in 2025, totalling over £1.1 billion, a 97% increase on the prior year. The UK accounts for 5.8% of global venture capital investment and consistently leads Europe, attracting more investment than France, Germany, and Sweden combined.

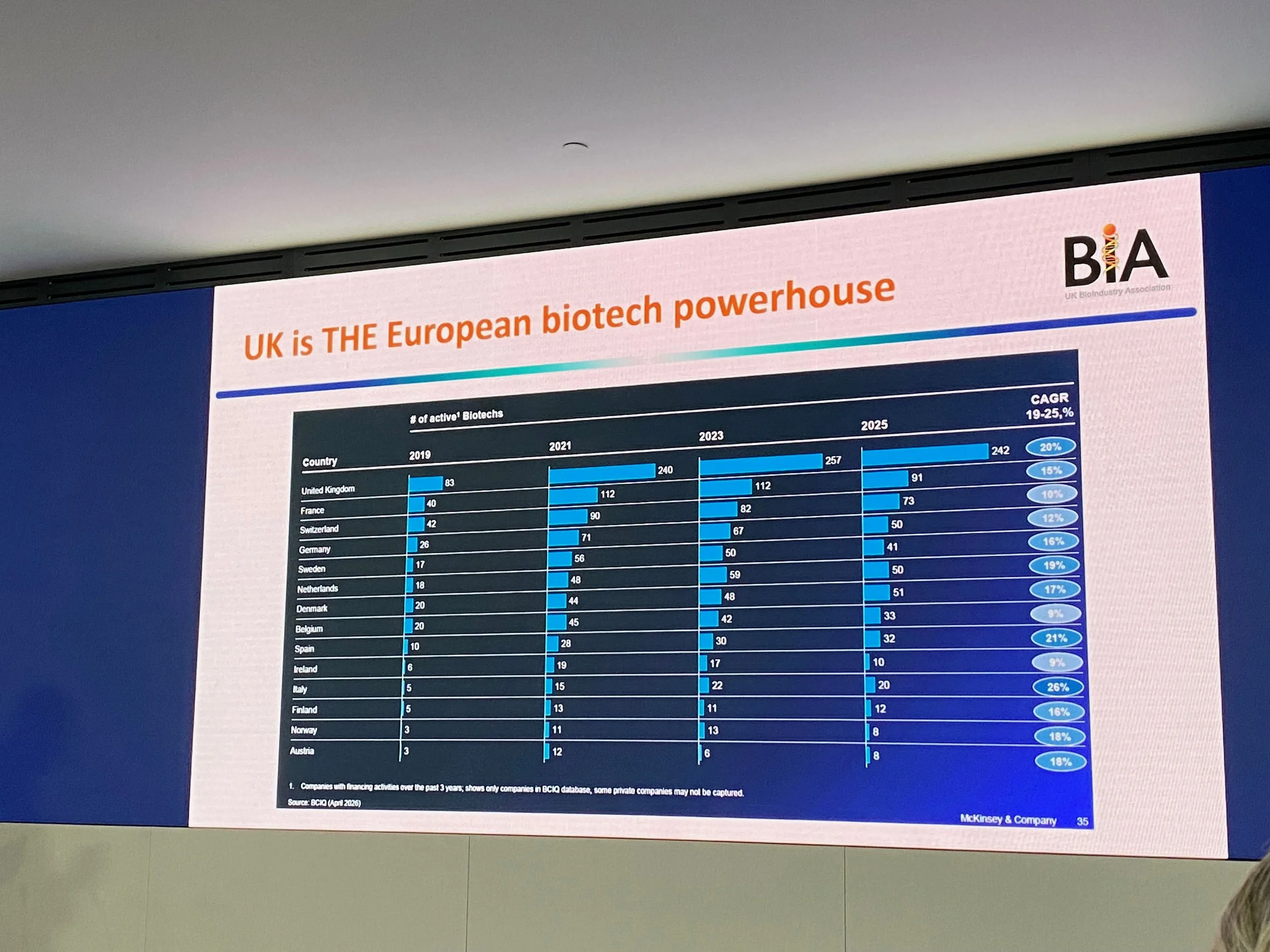

BIA: The UK is THE European biotech powerhouse

Professor Chris Molloy, CEO of the BioIndustry Association, who was speaking at the OFI Health Tech Showcase, laid this out with characteristic precision. The BIA, home to over 600 companies, published data at Bio Europe confirming what many in the sector know but few communicate clearly: the UK does not just invent. It approves drugs. It builds companies. It generates commercial returns.

The UK outperforms its nearest neighbours not just in publications, but in drug approvals and in the velocity at which we are creating investment opportunities. This is not a nursery nation. The data says otherwise.

What Has Changed and Why It Matters Now

The global environment for life sciences has shifted. Regulatory certainty, once taken for granted in some markets, is now an asset in short supply. Professor Molloy put it directly: “the UK is now one of the most stable regulatory environments on the planet, something we would not have said a few years ago, and something we need to say loudly now.”

That matters for two reasons. First, it is true. Second, it is an argument that international capital has not yet fully priced in.

Lord Vallance, Minister of State for Science, Innovation, Research and Nuclear, reinforced this from the government's side at the event. The Life Sciences Sector Plan, published in July 2025, is the most comprehensive statement of intent the UK has produced in a generation. It commits up to £520 million through the Life Sciences Innovative Manufacturing Fund, a £4 billion allocation from the British Business Bank targeting £12 billion in matched private investment, and a goal to lead Europe in R&D investment by 2030 and rank third globally by 2035.

Clinical trial reform is also underway. The target is to reduce commercial clinical trial setup time to under 150 days and lower, a number that will matter to global pharma when they are deciding where to run their next Phase II.

These are not ambitions. These are funded commitments.

New Plumbing for Private Markets

Tim Davies, Regional Head of UK Primary Markets at LSEG, brought something concrete: infrastructure news.

The London Stock Exchange's Private Securities Market launched its first transaction earlier this year under the PISCES framework, trading secondary shares in Oxford Science Enterprises. OSE, valued at approximately £1.3 billion, holds stakes in over 100 companies across AI, quantum computing, and life sciences. The PISCES/PSM structure now has around 23 to 24 liquidity providers, including investment banks, corporate stockbrokers, and platforms such as Crowdcube. Two or three more companies are expected to go live in the coming weeks.

This matters for a simple reason. One of the persistent friction points in UK life sciences investment has been liquidity. Institutional investors and family offices have been reluctant to commit to long-horizon, illiquid private company positions. PISCES, by creating structured, exchange-based, intermittent secondary liquidity, changes that calculus. The boundary between private and public markets is getting thinner, as one market participant put it.

Davies also highlighted a return of IPO activity. The first pure biotech IPO since 2020 completed in early 2025, with Rockfall Therapeutics raising £44 million through a reverse takeover. For those who follow market signals, this is not a headline; it is a green shoot.

And for those who attended the SFO Alliance's SFO Week in May, where single family office investors discussed life sciences and medtech allocation, the PSM/PISCES structure came up repeatedly. SFOs want structured access to private life sciences assets. They have capital. They want the infrastructure. The infrastructure is now here. All this helps how the UK is seen. Yet more can be done in terms for fiscal policy to incentivise UK corporates to invest in UK innovation and in changing the perception of how the UK is seen as a market that is rebuilding its regulatory architecture to support not just innovation but growth.

Flagship Pioneering and the Venture Creation Question

Lena Afeyan, Head of UK Science Strategy and Innovation at Flagship Pioneering, brought a different frame. Flagship does not invest in companies. It creates them. The model, responsible for Moderna among a portfolio of over 100 companies spanning AI-driven therapeutics, agriculture, and materials science, starts from a biological hypothesis, not a team.

Flagship's commitment to the UK is not a courtesy visit. The partnership with the Francis Crick Institute is a long-term structural play: Crick science, Flagship capital, and a systematic approach to transforming research into ventures. The annual Summer Fellowship is how Flagship builds its talent pipeline in the UK, embedding its company-building culture in the next generation of entrepreneurial scientists.

The model Lena described is, in essence, a different answer to the same question the rest of the room was circling: how do you close the gap between invention and commercial scale?

Flagship's answer is to redesign the creation process. The government's answer is regulation and capital. LSEG's answer is market infrastructure. The BIA's answer is narrative and advocacy.

They are all right. And they are all needed simultaneously.

The Question I Asked Lord Vallance

During the Q&A, I asked Lord Vallance directly: what is the government doing to incentivise UK corporates, not just overseas investors, to invest in UK innovation?

It is a question I care about because the data is stark. At the late stage, over 60% of UK venture funding already comes from overseas. In deals over £50 million, international investors are involved in over 94% of transactions. The UK is Europe's leading innovation ecosystem, but we are increasingly dependent on external capital to scale our own inventions.

Lord Vallance acknowledged this as a structural gap. The government is examining demand-side mechanisms to complement the supply-side infrastructure it has built. That is, as I see it, the diplomatic formulation of a real problem: UK pension funds and UK corporates are not backing UK innovation at the scale the ecosystem deserves and requires.

This is not a new observation. What is new is the urgency. The Mansion House Accord and the British Growth Partnership are beginning to redirect some pension capital toward UK growth assets. But corporate venture capital, the dedicated innovation investment arms of UK-based companies, remains structurally underdeveloped relative to the US, Japan, and other countries. Bear in mind what companies seeking investment often do not just need a cheque. Instead, what they need is sector knowledge and experience that many corporates have. The knowledge of how to commercialise the innovation that they have seen and can create value and growth.

The argument for UK corporate venture capital is strategic, not just financial. UK corporates that invest in UK life sciences innovation gain early sight of technologies that will reshape their industries, build relationships with the scientific community, strengthen their supply chains, and signal to government and the public that private enterprise is invested in national outcomes. The return is not purely financial. It is reputational, strategic, and political. And it is also reputational for the UK and how it is seen internationally by partner nations.

That argument needs to be made better, louder, and more specifically. And it needs to be made by people who understand both the investment landscape and the strategic advisory infrastructure that moves capital.

The Narrative Gap Is the Biggest Gap

Here is what I took away from the afternoon.

The data is good. The infrastructure is improving. The regulatory environment is more stable than it has been in years. The government has a plan. The BIA has the evidence. LSEG has the market plumbing.

What is missing is a coherent, internationally legible narrative that ties it all together.

When I in rooms and in conversations with a sovereign wealth fund, a corporate venture team, or a family office in Tokyo, Dubai or Abu Dhabi, Singapore, or Madrid, or even in the US, the UK life sciences story is not landing with the clarity and confidence it deserves. The instinct of international investors is still to default to the US for biotech and to assume the UK story is either too early, too small, or too illiquid.

None of those assumptions are accurate in 2026. But assumptions persist until someone dismantles them, deliberately, with data and credibility.

That is a job for strategic advisers, for people who can translate scientific and commercial evidence into the language of investor trust. It is a job for narrative architects who understand that perception, not just performance, drives capital allocation decisions.

It is the job I do.

What This Means in Practice

If you are a life sciences company preparing to engage international investors or access new capital pathways, including through PISCES, the PSM, or direct SFO outreach, the question you need to answer is not just what is your science. It is: what is your story?

Your story needs to be credible to a pension fund trustee who has never heard of your therapeutic area. It needs to be compelling to a family office principal in Hong Kong who is comparing you to a Flagship-backed asset in Boston. It needs to be confident enough to survive the scepticism of a CVC team at a FTSE 100 corporate that has never led an external venture investment.

Reputation and how you are perceived is strategic capital. It is the thing that makes a meeting happen, that keeps a conversation alive, that tips a decision toward yes. Building it requires the same discipline and rigour as building a clinical programme or a market access strategy.

The Office for Investment's event was a reminder that the UK has the knowledge, the science, the infrastructure, and the political will to become the global benchmark for life sciences commercialisation. The next step is the story.

“We have a podium place in biotech. The question is whether the world knows it.”

Professor Chris Molloy, BioIndustry Association.

They will. If we tell them.

A Note of Thanks

I am grateful to the Office for Investment Venture Capital Unit for the invitation to attend and participate in this showcase. The quality of the speakers, the seriousness of the companies presenting, and the calibre of the investors in the room were all evidence of a sector that is moving and an ecosystem that is evolving. Events like this matter because they create the collisions between science, capital, and policy that innovation ecosystems need.

The UK has an extraordinary story to tell. Let us work together to tell it better.